Two buddies Akbar (Head – Logistics) & Antony (Head of Production) go way back in their friendship are now working in the same company.

Among both Akbar was the smarter one and Antony was the conservative one in a position above Akbar. Akbar knows in & out about the industry and knows processes that can be exploited in the company to take advantage of. Understand the processes of the company, then go on to understand how the fraud was performed, and how was the same identified by the auditor.

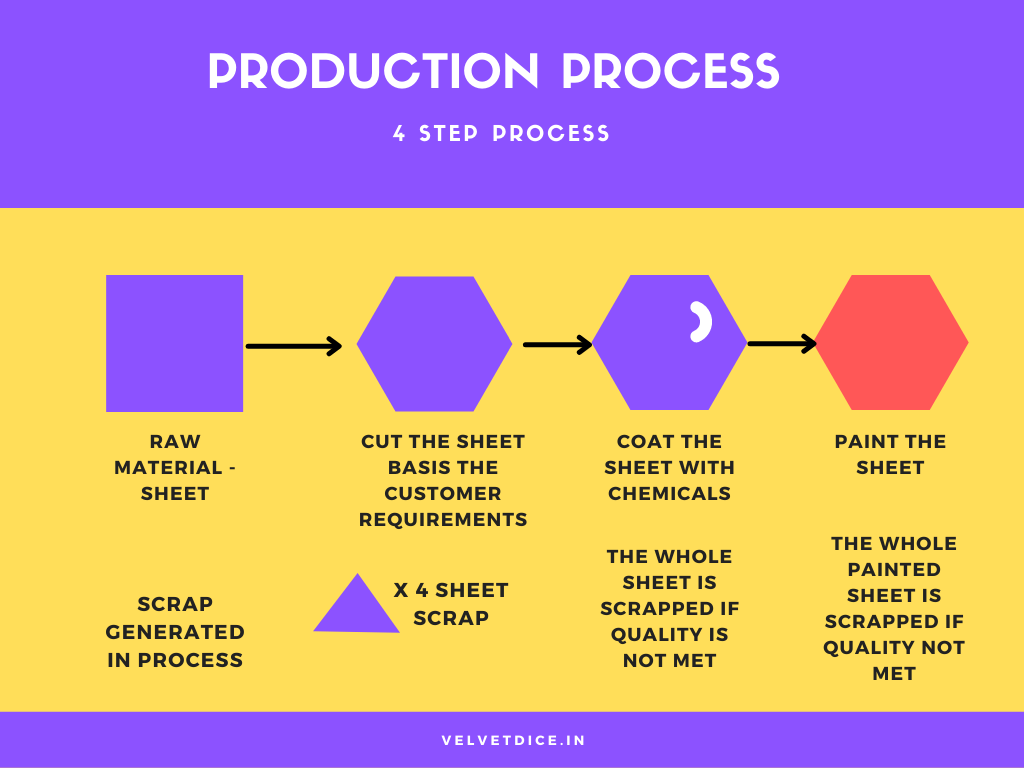

Part 1: The Production

The production process of the plant had three separate but continuing processes where the sheet would first be cut according to the requirement of the customer, then be coated and at the end be painted. When the input sheet went through the cutting process it had to be cut into specific dimensions and the balance portion of the sheet would be put under waste. The plant has a barcode system where each sheet has a barcode that is scanned at the end of each process to account for WIP & FG.

A sheet that was disposed of at the first stage would fetch the maximum value, the coated sheet (stage 2) a little lesser and the painted sheet (Stage 3) the least. For the sake of understanding consider the following sale price per unit:

Sheet – $ 100

Coated Sheet – $ 20

Painted Sheet – $ 5

All the cut portions, rejections were moved to the scrap yard and the scrap yard had three segregated yards for the workers to drop the scrap basis the point at which the scrap/rejection happened.

Part 2: Manpower

The company usually had manpower services outsourced as the production required people that had to do mundane activities and it was comfortable for the company to outsource it to manpower services rather than having employees of their own.

The vendor deployed close to 30 people, and they were utilized at different parts of the plant – in the production, maintenance, scrap yard, transportation etc. So the contracted manpower would be responsible for the movement of the sheets inside the factory and it was their responsibility to move the cut sheets to the scrap yard.

Part 3: Scrap Sales – Buyer Selection

The company had a process of obtaining 3 competitive bids for scrap sales and would then get the vendor approved by the Head – Production & the Finance Manager. The responsibility of obtaining three or more quotes and lying with Akbar & the approval lied with Antony & the Finance Manager.

When the scrap materials are removed, the security at the gate has to physically verify what’s sold and be there when the weighment of the scrap is performed.

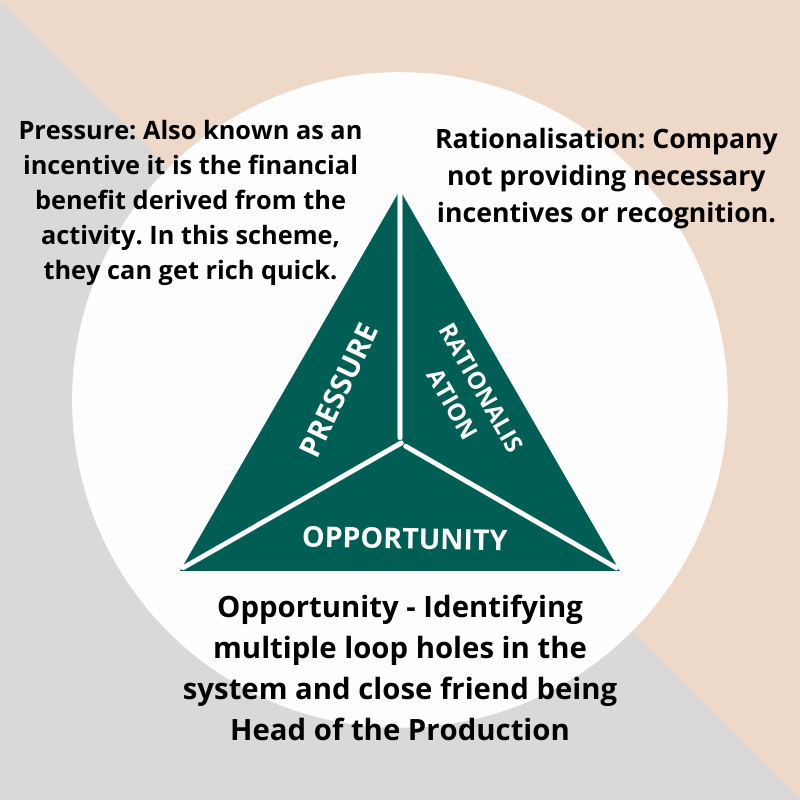

Akbar sketched out a plan, that required help from multiple people and Antony being a close confidant helped get the necessary approvals inside the system without people getting any doubts.

Scheme of Fraud:

- The perpetrator obtained three scrap buyers quotes out of which two were fabricated by the buyer who was arranged by the perpetrator himself. Meaning, buyer – A gives three quotes (for A, B & C) from three different addresses one of which is legitimate on his own but the other two prepared by himself. He also ensures that the rates that are given are slightly lower than the market rate so that the profits that he can make in resale be higher (and a cut from this can be given to the perpetrator for providing the order to him)

- The perpetrator now contacts scrap buyer A’s brother who is a manpower supplier to supply manpower to the plant for production & scrap handling.

- These contract labourers are informed prior hand to drop some of the sheet cuts into the coated or painted sheet scrap yards so that higher price scrap can be bought at a lower price and sold in the market.

- The perpetrator now speaks to the only security among the 6 security guards who had agreed to not physically verify when scrap sale happens.

How did the Internal Auditor find it out?

- Understands the Input-output ratio at each stage of production and theoretically now calculates with the production date. If there was a sheet that was 10 kgs in weight and has a 30% wastage in the process, then the sheet scrap to be sold would be 3 kgs. The theoretical weights arrived basis of the I/O ratio was compared to find out variances.

| Particulars | Theoretical Quantity (Kgs) | Quantity Sold (Kgs) | Variance (Kgs) |

| Sheet | 1000 | 600 | 400 |

| Coated Sheet | 500 | 600 | (100) |

| Painted She | 400 | 700 | (300) |

- Verified the scrap buyers’ quotations and called the phone number, checked Google to find out the existence of the company and then visited the locations of the scrap buyer’s basis the address given in the quotations only to find out only one quote had a small yard, the other two addresses were empty land.

- After further speaking to some people from the contract employees, the information on the owner being the brother of the scrap buyer was found out.

- Did a surprise verification of the scrapyard to find out some of the sheet scraps were also noted in the painted sheet scraps.

- Cross verified the presence of the security guards with the scrap sale time to find out that there was always the same security guard who was responsible for physically verify and letting the truck with all the scraps be cleared from the plant.

All these evidence were quite persuasive enough to interrogate the perpetrators.

Fraud Triangle:

Perpetrator Response: “I was not aware of this” was what Antony had to say and Akbar claimed himself not guilty throughout the process and blamed the system.

Questions to ponder upon:

- Why didn’t the management review the organisation structure on a periodic basis?

- Should the Finance manager be being one of the approvers of Scrap sale vendor been more proactive in knowing about the buyers that were shortlisted by operations personnel?

- Had Akbar asked Antony to change the input-output ratios, would it have been possible to detect this?

Happy Reading! Until next time!

Leave a Reply