John, a classy & fearful plant manager at most times dons the people around with his sharp & manly voice tone sometimes even dominated the plant head with his arguments.

John has close alliances with all the plantations nearby and it has a diplomatic relationship with the extremist groups that threaten organizations in and around the place to obtain funds to promote their agenda in the place. John tells crazy stories of Kingpin Z, head of the group who’s quite ruthless when his ransom demands aren’t met.

Part 1: Vendor Selection

As a plant manager, John was responsible for the purchase of Coal that will be used to burn the furnace for the production process. As per the company policy, a minimum was of three quotations need to be obtained and vetted, and whenever there is a price increase above 20% then the same process is repeated. John had obtained the three quotes and arrived at a vendor who was supplying coal to the plant for 2 years even when the price went above 20% of the initial price. However, this was discussed and agreed with the Plant head.

Part 2: Good Receipt

The coal was dispatched in trucks to the plant and for the majority, the trucks usually arrived after the usual office hours to avoid halting production during the peak hours. Trucks get physically verified at the entry by the security guard, goes to the weighment yard, obtain the weighment slip which is printed in triplicate, one for the weighbridge, one for the vendor and one for the accounts payable team.

Part 3: Consumption

Consumption of coal is booked basis a ratio that was arrived at basis historical data. If 1 ton of finished goods is produced, then 1 ton of coal is booked for consumption in the books. This ratio was changed to 1.2 tons of coal per ton of finished goods to cover up the excess quantity received as per the books (but not physically available).

Part 4: Accounts Payable

Accounts payable was handled by retired personnel who was working there due to family constraints and was struggling to meet ends financially. I guess it’s clear now that John had a dominating hand when it came to approving the invoice by the accounts payable team.

Scheme of Fraud:

- John gets the rate increased after the initial rate is increased, which then does not go through the same approval process again.

- John now lets the truck do the weighment twice; if a truck carries 10 tonnes then 10 tonnes are weighed and at the coal yard only 8 tonnes are removed from the truck and later the left out 2 tonnes is weighed making it 12 tonnes for billing but physically only 10 tonnes present at the yard.

- Now the consumption ratio is changed from 1 to 1.2 tonnes per ton of output produced to burn the excess quantity that is now sitting on the books.

- Invoice revision is now done after the weighing is done as the initial invoice while entering the plant would be 10 tonnes and now a revision is made to 12 tonnes and the excess billing is done which is later approved by the Accounts payable team as there is sufficient evidence for them to process the payment and the approval lying with the plant head who doesn’t vet as much as the AP team does.

How did the Auditor find it out?

- Expense comparison from the prior period to the current period along with the output production.

- Checked the weighment slips which had the same truck weighing in under 30 mins gap.

- Most of the time the same set of trucks came in, and the details of the truck were not recorded at the entry gate by the security.

- CCTV camera that has been placed at the weighbridge is monitored to identify if the same truck is weighing twice in under 30 minutes.

- Consumption ratio of coal changes from 1 to 1.2 from the prior period to the current period.

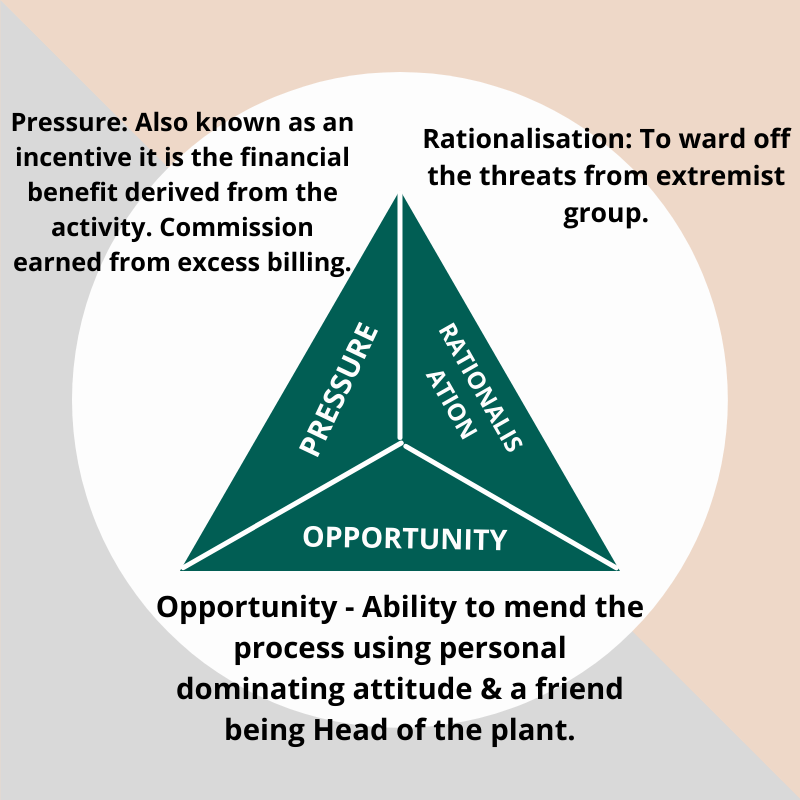

Fraud Triangle:

Perpetrator response: “Certain things are beyond your understanding; we have to do certain things to keep peace at our workplace” indirectly meaning this is an agreement that is made with the extremist group for their functions to work orderly without any interference from them.

Questions to ponder upon:

- Could it be possible that the perpetrator was doing fraud to keep things functioning in a peaceful manner without intervention from the extremist group at the Plant?

- Can a person be above the system just by placing his dominating attitude? Why are people at lower levels scared to make the whistleblower call?

- Is it better for the perpetrator to change the consumption ratio or write off the excess quantity as an abnormal loss with approvals from relevant authorities? Would it still ring as a red flag?

interesting read.thanks.